|

Efficiency & Convenience: Summary: The length and importance of this Views justifies a brief summary, so we begin with those summary points for those who don't have time for the full issue. Efficiency and convenience are the flip sides of the same coin, that created retail at the dawn of history, with vast increases over the past 100 years. There is good reason to believe we are on the verge of a five-fold acceleration of efficiency, convenience and retailing! The economic division of labor created the need for the largest industry in the world, retailing, thousands of years ago. The basics of the process changed little over millennia, until the early 1800s, with the Birth of Plenty (Bernstein) in England, leading to a century of massification. Mass production, and mass distribution led to mass retailing - self-service. This led to a "new" business model for the world's first billion dollar business, of low margins and limited capital to deliver massive efficiency (and sales,) with A&P at the forefront. The resulting "creative destruction" (Schumpeter,) revolutionized the supply chain and forced efficiencies in manufacturing, but created massive opportunities for growth in both industries. Shoppers loved the exploding assortment of high quality merchandise at plunging prices. Retailers became merchant warehousemen who managed the logistics of stores and supply chains, with shoppers self-managing the sales process. Decades after A&P's hey day, Walmart picked up the efficiency baton and created the new "world's largest business." "Selling" was redefined in retailers minds as price-promotion - paying shoppers to buy. Brand suppliers cooperated with this in-store approach, and moved their own "selling" to mass media, radio and TV. Mass media is emasculated selling, since it cannot "close the sale," which is done in-store. PathTracker®, beginning in 2001, showed the relationship between efficiency (and convenience,) and total store sales. Amazon's "sell just one" (of 50 million) has driven their sales, but two of the most successful bricks-and-mortar retailers are using the same thinking to deliver multiples of their lesser colleagues sales. In the end, the mother lode of efficiency in self-service retailing is the unconscious efficiency of the shoppers themselves, on the sales floor. 1. The division of labor created retailing Retailing is the world's largest industry because it is the intersection of what everyone produces with what everyone else needs. This lies at the root of my oft saying that, "retailing is the cutting edge of social evolution, always has been and always will be." But here we want to focus on the fact that retailing is at the cutting edge of efficiency and convenience. First, in the beginning, society soon learned that some people were better at some things, and other people were better at others. This fundamental fact of being, meant that society could self-select (freedom) with the labor of society being divided up with individuals producing what they were good at. Of course, this division of labor forced the creation of a means of exchange of one another's production, hence exchange, trade, markets, of which retail is the largest, and touches everyone directly. To understand retail it is essential to understand that its foundation is in the efficiency of society. I have added the term convenience to efficiency, because efficiency is a colder, more objective expression of the warm convenience we personally and subjectively experience by having our own desires and needs met at retail. That is, efficiency is what retail delivers, while convenience is what shoppers receive. These concepts have trillions of dollars of impact, annually, today. That impact has swelled over the past 200 years, and the swelling is far from over. 2. A century of massification There are four pillars of prosperity, essential for societal growth:

All four of these first occurred simultaneously in English society in the early 1800s. The first two of these principles relate to the freedom of our persons and minds, and the latter two address the freedom of our interaction with the rest of the world. It is these latter two that address most closely the retail marketplace. The simultaneous occurrence of all four of these principles accelerated a century of massification:

Again, bear in mind that mass production is simply a matter of somebody carrying to an extreme their own special competence at producing something, whether "shoes or ships or sealing wax." The thing that makes this effective for society is that now, rather than inefficient production of tens or hundreds of items of possibly inconsistent quality, thousands or millions of quality items could be produced efficiently. But such efficient production would be of little use without the means of mass distribution, initially greatly facilitated by steam power (rails, ships,) roads, docks and warehouses. These, in turn, served an exploding number of retail outlets - probably upwards of two million neighborhood "mom-and-pop" stores in America in the early part of the 20th century.

3. Enter: Self-service retailing For thousands of years, retailing made few conceptual changes, with the exchange of goods and payment being made from the hands of the retailer to/from the hands of the customer. In this scenario, there was a genuine opportunity for personal selling skills to oil the efficiency and convenience of the transaction. This millennia long state of affairs we might reasonably call the first wave of retailing. Self-service ushered in the second wave of retailing, which has dominated the past century. We will discuss this second wave in some detail, because knowledge of its driving principles, and ramifications for all parties - shoppers, retailers and their suppliers - are often not recognized by the parties, to the detriment of efficiency and convenience. Moreover, there is now a third wave of retailing which is already beginning to flood the scene, offering massive, further increases in efficiency and convenience. "A grocer named Clarence Saunders... opened the country's first self-service food store, Piggly Wiggly, in Memphis in 1916,..." (from Levinson) Clarence Saunders played an important intellectual role in the early days of self-service, specifically focusing on how to allow the retailer to carefully manage the sales process under self-service conditions. [See: Sorensen, The Path to Purchase is Often a U-Turn.] It is clear that Saunders focus was on efficiency. However, his concerns were virtually swamped by an avalanche of efficiency, with A&P in the van. Some minimal understanding of the history of A&P, that grew to be the world's first billion dollar business, is necessary to understanding the economics of self-service retailing today. The company's roots go back to the time of the Civil War, and it's founder, George Gilman, who was an aggressive and creative salesman, at least 50 years before self-service got underway. "Being a tiny tea dealer did not satisfy George Gilman's ambitions. After taking a couple of years to learn the business, he struck out on a radical course, establishing himself as a marketer of no small genius. First came a new name. At some point between June 1861 and early 1863, Gilman & Company became the Great American Tea Company-a startling departure from the universal practice of merchants putting their names on their businesses... In the most nontraditional departure of all, Gilman began to advertise massively... The advertisements... repeated a phrase that was to become a staple of Great American's advertising for years to come: 'ALL TEAS sold at TWO CENTS PER POUND PROFIT.'" (from Levinson) This fixation on a low margin carried forward into the evolution to self-service half a century later, when the two sons of Gilman's early associate, George Hartford, drove the long and unremitting growth of A&P into the 1950's. Before moving to this self-service phase of A&P, it is worth noting that A&P introduced their own branded and pre-packaged tea, Thea Nectar. "A brand-name tea was an extraordinary product to bring to market in 1870... The widespread sale of brand-name foods in sealed packages was still two decades in the future." (from Levinson)

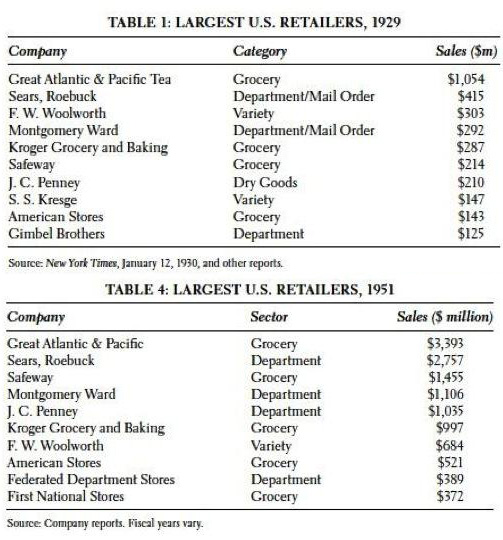

The generation of A&P management following this exhibited the same type of visionary marketing genius, paired with attention to financial detail that presaged the finest cost accounting, of the type that would come many years later with the advent of electronic computers. 4. A commitment to low margins In practice, self-service retailing, beginning in the early 20th century, profoundly altered retailing, massively increasing both efficiency and convenience. The driving force behind this efficiency was the absolute commitment by A&P to low margins and high volume. Low margins and high volume are economic measures of efficiency. As John Hartford testified at trial, in 1945, "We would rather sell 200 pounds of butter at 1 cent profit than 100 pounds at 2 cents profit." (from Levinson) This was simply articulating the principle George Gilman, the founder of A&P, established some 80 years earlier. John Hartford, the marketing genius of the two brothers who drove A&P to become the first billion dollar business, in the 1920's, was "open to new ideas, but always insisting that lower prices would make more money by bringing more customers in the door... If the company's profit margin widened, it would be not a good sign but a bad one, an indication that A&P was forsaking the cost discipline that would lead it to domination of the grocery market." (from Levinson) This insistence on low prices as a consequence of low margins, was so extreme that a store manager delivering too high a margin from his store would be reprimanded! A&P's profits were driven by a focus on return-on-investment (ROI,) rather than margin. It wasn't just volume driving profits, it was low capital investment as well. For example, short term leases on stores not only kept capital investment low, but provided great flexibility in managing real estate through the turbulence of two world wars and the Great Depression. Without the capital deployment, properties could be terminated and new ones leased with minimal financial disruption. Also, low margins/prices kept turns high, and stagnation of inventory at a minimum. But A&P's efficiency didn't happen in a vacuum. You can see from these tables that they were not the only ones driving efficiency and benefitting from the move to self-service retailing:

These tables (from Levinson,) give you some idea of the players and their relative magnitude. What this does not show, directly, is the devastating impact on the grossly inefficient Mom-and-Pop stores, nor on the distributors that served those stores. The entire retail industry was very inefficient (and inconvenient to shoppers,) in the early part of the 20th century. Costs of operations were high for retailers, distributors, and their manufacturer suppliers. This translated into high prices for shoppers. The food budget alone was one third of a typical household's costs, and homemakers spent an inordinate amount of time shopping in a very large number of very small stores with limited selections of merchandise, often of poor quality. The unrelenting focus on thin margins, and high volumes with minimal use of capital, drove massive increases in efficiency, with wins for all surviving parties:

The benefits of self-service were a significant factor in the social evolution of the first half of the 20th century. At the same time, it played a major role in the "creative destruction" that vastly pruned and realigned "Mom-and-Pop" retail and the crazy quilt of antique distribution that supported those outmoded operations. "A contemporary of the Hartfords, the economist Joseph Schumpeter, coined the phrase 'creative destruction' in 1942 to describe the painful process by which innovation and technological advance make an industry more efficient while leaving older, less adaptable businesses by the wayside. For the economy as a whole, creative destruction is enormously beneficial, permitting a shift of labor and capital from sectors where less is required into areas where new products and services are in demand. It is precisely such shifts that make economies grow. For many individuals and many communities, on the other hand, creative destruction is painful, entailing business restructuring, job elimination, and the disappearance of companies and industries that have provided the economic base for a particular town or an entire region. Whatever its advantages, economic change inevitably leaves major losses in its wake." "In the first half of the twentieth century, the Hartfords turned their company into one of the greatest agents of creative destruction in the United States. Although shifts in the way the world buys food are far less heralded than innovations such as cars and computers, few economic changes have mattered more to the average family. Thanks to the management techniques the Great A&P brought into widespread use, food shopping, once a heavy burden, became a minor concern for all but the poorest households as grocery operators increased productivity and squeezed out costs. The proportion of workers involved in selling groceries plummeted, freeing up labor to help the economy grow. And the company's innovations are still evident in the supply chains that link the business world together. Although the Hartfords died decades before the invention of supercenters and hypermarkets, they employed many of the strategies-fighting unions, demanding lower prices from suppliers, cutting out middlemen, slashing inventories, lowering prices to build volume, using volume to gain yet more economies of scale-that Walmart's founder, Sam Walton, would later make famous." (from Levinson) In the tables of retailers above, Walmart is not represented because the latest table is for 1951. But notice that in both 1929 and 1951, Sears was number two, right behind A&P. Sears played its own significant role in "creative destruction" in the non-grocery trade, and was supplanted years later, in turn, by Walmart. Walmart began in the Sears-space, but expanded into the grocery-space, which, in turn, led Walmart to become the world's largest business, larger even than all but a few of the very largest countries, in economic terms. But the game changes - see the third wave of retailing below. [George Will, The Inexorable March of Creative Destruction.] 5. The "mind" of self-service retailing The societally changing phenomena of self-service retailing may have been driven by the Gilman/Hartford strategy of low margins and profits through volume, but it led to major changes in the thinking of the largest industry in the world. Up to this point in history, retailers were personally the nexus between those who produced and those who consumed. With self-service, literally, "shopper, sell yourself," the connection to shoppers was, if not severed, severely attenuated. The successful self-service retailer would no longer be the one with an intimate personal relationship to shoppers. In fact, clumsy efforts by a retailer to mechanically develop such a relation led one shopper to declare, in 2011, "I'm not here to enter into a relationship. I just want to buy something." The net result of self-service, this new-in-the-20th-century phenomena, was that retailers became merchant warehousemen, very nearly totally supply chain focused, with their connection with shoppers strictly mediated by a count of how much of this or that shoppers sold themselves in the stores. Very early this mindset became imbedded in the world's largest industry with the mantra, "Pile it high, and let it fly." No wonder a recent (2010) significant book is titled "The New Science of Retailing" and is focused on supply chain management. This supplier-facing mindset was accentuated by a revolution in thinking about "selling" to shoppers. If A&P was in the van of retailers driving the move to self-service, P&G was in the van of suppliers promoting and benefitting from it. [See Rising Tide: Lessons from 165 Years of Brand Building at Procter & Gamble,] The growth of branding, as shown by A&P's Thea Tea, and the movement from Gilman & Company to the Great American Tea Company, precursor to A&P, was originally as much a retailer phenomenon as a manufacturer phenomenon. In fact, retailers have always been more likely to step across the line into manufacturing and distribution, than manufacturers have been to do the reverse. One fundamental reason for this has been the retailer's focus on volume ("reach" to customers,) over margin, and the manufacturer's preference for margin. But then, the retailer has the customers, NOT the manufacturer. 6. So who's "selling" to the shopper? In fact, with the advent of self-service retailing, the whole concept of "selling" morphed into something that would be totally unrecognizable to a true personal sales person. [See: "How to Close Every Sale" (Commentary on Joe Girard's book),] However, retailers took one approach to the problem, and brands took another, with very important consequences for both. For the retailer, selling and promoting became nearly synonymous, and promoting almost invariably involved paying the customer to buy! That is, cutting the price. This made/makes a lot of sense, given the nearly overwhelming drive of retailers to increase their reach to the customers, as demonstrated by traffic. Other than marking things down at the shelf, with notices on the shelf, the two most prominent means of letting shoppers know about their price promotions was through splashy newspaper ads, and closely related weekly flyers - usually distributed along with newspapers. But since paying for newspaper ads was an added cost, it made sense to do it cooperatively with the suppliers of the products being promoted. This is the reality that survives to this day for grocery retailers: razor thin margins, if any, on many supplier products sold, with actual profits made from promotional funds raised directly from the suppliers, for the promotion of the suppliers products, whether through in-store placement/promotion, or any form of advertising featuring a brand supplier's products. Hence, the number one source of profits for self-service grocery retailers is supplier allowances, promotional fees, etc. And thus comes the proper recognition of these businesses as merchant warehousemen, seeking profits from others for making use of their high-traffic neighborhood boxes. This accounts for the overwhelming, backward focus on the supply chain, and scant knowledge of how shoppers behave in their stores, other than which items that disappear from the shelves, and need restocking. But let's be clear: this specific business model led to building, successively, two number one global businesses - first A&P and a few decades later, Walmart. (The Walmart model did have, initially, significant differences.) And these businesses achieved this status because of their overwhelming efficiency in operation driving convenience and low prices for shoppers. Walmart's efficiency, and the efficiency forced on their supply chain, has resulted in the typical household in America saving $2,500 per year, even if they never shop at Walmart. The efficiency improvements in the supply chain redound to the benefit of other retailers and non-Walmart shoppers as well. This leaves for consideration, other than cooperating with their retailer customers with their promotions, how could brand manufacturers "sell" to their customers? Bear in mind, that even if a retailer was national, each of their stores was local, as were the local newspapers. For the brand manufacturer, their need was to differentiate their own brand(s) from what was often vigorous competition, side-by-side in the stores, and to transcend all the stores where they had distribution, not just this or that retailer. Moreover, their business model was not volume at nearly any cost, but volume against the competition, and maximum margin achievable, within the competitive circumstances. As a consequence, national brands needed national media. 7. Mass Media The development of radio, and later of television, may have had a lesser and later impact on society, if someone hadn't funded their rapid growth. One significant source of that funding was the major brands' sponsorship of programming, such as soap operas, sporting events, news, etc.

The significance of this move by major brands to "selling" through mass media (massification of communication) can hardly be overstated. Not only did it provide funding for the evolving national media, it increasingly knit what might have been disparate regions of the country into a unified whole - national consciousness. The fact that retailing was the unwitting and unintentional force behind this does not detract from the fact that retailing was certainly at the cutting edge of social evolution for the past century. In a sense, efficiency and convenience are the glue that binds the United States together, and the glue of commerce will work its will on the global population regardless of political forces to the contrary. [See: Retailing: the Trojan Horse of Global Freedom and Prosperity.] For our purposes, it is important to note that selling that had occurred at retail, pre-self-service, was now ensconced in the national media, with the power driven by the troika: brand manufacturers, advertising agencies, major networks (radio and television.) But one baleful deficiency came to be overlooked. Any professional salesman lives for the final moment of the sale, when it is consummated in the close! Hence, the mantra, close early and close often. Unfortunately, it is not possible for even the most super "selling" mass media to actually close the sale, being remote from the location where the sale will be consummated. 8. Enter PathTracker® The non-selling of both retailers and their brand suppliers began to be starkly apparent when trying to understand their sales efforts in relation to shoppers' actual behaviors in stores. Beginning in 2001, detailed knowledge of shopping trips on a second by second basis identified the gross inefficiency of shoppers in selling to themselves. Slowly, it became apparent why no one was actually selling in the stores - retailers looking to the supply chain, brands looking through tunnel vision at the brand-on-brand mayhem in the aisles of their categories, and shoppers with willy nilly inefficiency in stores quite inadequate for the purpose. It reminds of Churchill's comment on golf, "Golf is a game whose aim is to hit a very small ball into a even smaller hole, with weapons singularly ill-designed for the purpose." We might paraphrase the latter part of that quote as "shoppers are shopping in stores that are singularly ill-designed for the purpose." And what is the evidence of this? Up to 80% of the shoppers time in most stores is wasted on wandering and unproductive search. [See: Sorensen, "The Science of Shopping," and Hui, Fader, and Bradlow, "The Traveling Salesman Goes Shopping: The Systematic Deviations of Grocery Paths from TSP-Optimality." The proof of this is not only in the confirmed studies of millions of shoppers on a second by second basis, but in the proven success of a few retailers turning a major portion of that lost time into sales. It turns out that the third wave of retailing lies in massive increases in efficiency, not of manufacturing, distribution or even store operations, but rather in the efficiency of the shopper - which of course can be influenced by store operations. But in order for that to happen, retailers must understand a good deal more about how shoppers shop and purchase on a second by second basis. They must become as obsessed with their squandering of shoppers' time, as they have been with inventory, and sales per square foot. Dirt is cheap, shopper's time is gold! Efficient use of their time, is perceived by shoppers as convenience. As long as a major global retailer can say, "Why would we do this, if no one is paying us to?" - or a major global brand can say, "All I need to know, is which should come first, the dog food or the cat food?" the potential for massive increases in efficiency, driven by shopper efficiency, are an open door for sales and profits to any retailer or supplier who breaks out of the pack through learning about shopper behavior, and leveraging that knowledge. For perspective, it is important, not to ridicule the attitudes of retailers and their suppliers, but to understand, first, that it is exactly these attitudes that have driven the efficiency of retailing, to the benefit of shoppers world-wide, over the past 100 years. Secondly, these attitudes serve as the bed-rock, or foundation of profitability of what comes next. Those who win the future are likely to be those who execute well now, but sink their gold mine of efficiency in a new mother lode. 9. The Third Wave of Retailing So this brings us to the current transitional period, while most of the world of retailing is intellectually stuck in what happened over the past 100 years, even though major elements of the next wave are already lapping the shores. What I have attempted to do here is to force attention to the causative element behind the evolution of retail: efficiency and convenience. One would have to live behind the door to not recognize the growing impact and potential of personal electronic communication on shoppers. In fact, there will be a continuing Convergence of Online, Mobile and Bricks-and-mortar retailing. I refer to this as C-O-M-B retailing. (For all of my RetailWire comments on COMB, search for COMB at this link.) But a great deal of the millions of dollars being invested in this currently is misguided, through a misunderstanding of what the real inefficiency problems are in shopping. At the same time, there is in our midst someone of the genius qualities of their predecessors, the Gilmans, Hartfords and Waltons. I speak of Jeff Bezos of Amazon, and cite, not the incredible growth and success of the business, but this statement from someone who worked with Jeff while the foundation of growth was still being laid: "We used to joke that the ideal Amazon site would not show a search box, navigation links, or lists of things you could buy. Instead, it would just display a giant picture of one book, the next book you want to buy." "One book, the next book you want to buy!" This is the sheer genius of a salesman, not to ignore the 50 million books he has on tap, but to realize that his job is to sell just one! And then, to consider selling another, and then another, and another, until the shopper is sated, for now. This is the "efficiency process" that self-service bricks-and-mortar retailers have almost totally ignored, and which is the key to massive increases in sales and profits in the third wave of retail. You can find my suggestions on this process for the current bricks-and-mortar stores in the most recent ten issues of my Views, but especially these two: I have been citing two retailers who are successfully delivering super efficiency/convenience to their shoppers for several years. I'm quite certain that for neither of these retailers was this a matter of happenstance. Stew Leonard cited path and selection in his book, and there is nothing accidental about Costco's path and selection practices. In some ways it is unfortunate that both of these stores are "limited" selection stores. The reality is that Costco has certainly demonstrated that a proper single path can be managed in a grid type store, something that could be managed in a Walmart super center without major alterations to the store. Gaining the efficiency of a limited selection in a store with a huge selection is addressed in the first of the Views cited immediately above. But then again, as the quoted retailer said, "Why would we do this if no one is paying us to?" Indeed!

Here's to GREAT "Shopping!" |