Maybe the title here should be, "The 'Path-to-Purchase' Ought to Be a U-Turn." But that's getting ahead of our story. The reality is that when shoppers enter a store, they will often make their way, early in the trip, to the back of the store. At that point, most often they will turn left and shortly thereafter, take another left, and return to the front of the store for checkout and exit - effectively creating a U-turn path.

Of course that is not the only path, but it is more common than might be thought. And why not, when the single most common number of items purchased in any store in the world is ONE! Half the trips to a drug store purchase three or fewer items; half the trips to a supermarket purchase five or fewer items. This means that a simple and short path really is adequate for most trips, so shoppers will, if at all possible limit themselves to that type of path.

Now these are facts that the brand supplier and retailer can either leverage to their profit, or dismiss as irrelevant to "our target customers." It's usually more profitable to work with the shopper than to try to get them to work with you. Shoppers shop this way, not because they want to, or have made a conscious decision to do this, but because it instinctively fits their own needs. Probably they are not even aware of it. In fact, shoppers are as poorly informed (aware) about their own behavior, as are the people asking them about it.

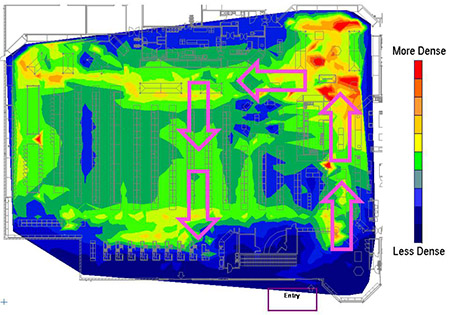

Before we look at a way to make money with this knowledge, let's look at a common retail strategy that kills profits. You will notice in the above store how that shoppers enter the store near the right side of the store, and there is heavy traffic from that point (on the right,) back through a broad aisle bounded by the service deli and service bakery, to the well lit and bright produce area in the right rear of the store. This aisle accounts for a significant proportion of the stores sales and profits.

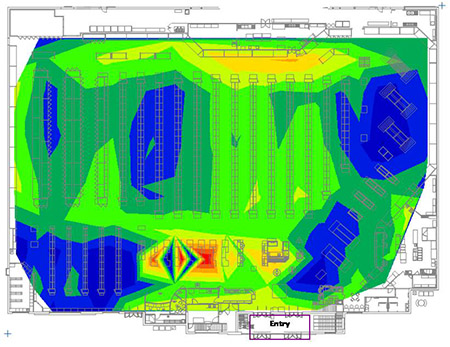

Now let's look at another comparably sized store. In the store at the right, again you have the service deli and service bakery leading into the produce, which is aligned up the right side of the store. But notice the dearth of traffic in that area. The entrance is center-right, more or less right at the front of the most attractive area of the store. Then why is the traffic moving to the back of the store in the center-of-store aisles to the left of produce? Having the doorway as far toward the center, instead of nearer the right is a contributing factor. But here is a scene you will see in the entrances of stores - and many other places:

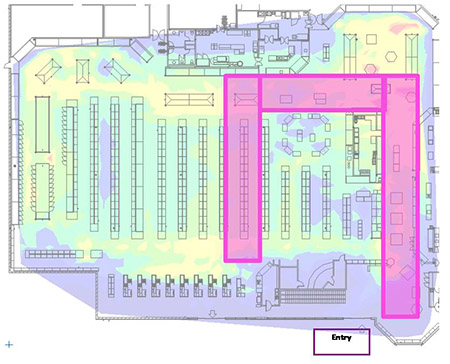

The produce is there, off to the right, well barricaded behind various and sundry displays and signs pushing a variety of merchandise, all NOT produce. Although this photo is not from the same store, these two stores and tens of thousands of others are possibly unwittingly creating artificial barriers to where they really want shoppers to go, essentially suppressing sales and frustrating shoppers. Faced with the entry above, this third store is getting major flow to the back of the store through the center-of-store aisles to the left of produce, just like the second store is.

These are not isolated instances, or minor independent stores, but major national and regional U.S. supermarket chains. They, and many others, freely violate the principal that shoppers are attracted to open spaces. That's why they shop mostly on the perimeters of stores and avoid those steel canyons crammed together in the center of the store. It is NOT solely a function of the attractiveness of the merchandise. The top selling Costco manages to regularly move a million dollars of merchandise per day. A major factor in their stores is the huge open area, bazaar-like, that dominates the center of the store, with the "steel canyons" innocuously and conveniently arrayed within ready eye-shot, accessible but out of the way, around the perimeter.

But, enough on the sins at retail. An old Chinese proverb says, "better to light a candle, than to curse the darkness." So, back to our observation that "the path to purchase is often a U-turn," or as we will see, at least ought to be a U-turn. And by "U-turn," we mean that often the early part of the shopping trip is the shopper making their way to the back of the store, a left turn for one or a few aisles (usually to the first few that return to the checkout area,) and then that second left turn that returns them to the front of the store.

Knowing that this is common, retailers ought to make that easy, and define the path for the shopper, deliberately, rather than leaving to chance (and possibly ignorance,) of just what the dominant path is. We can illustrate this as on the left here. Since we already know that shoppers have a natural proclivity to follow something like this path, let's help them by removing ALL displays and placements that block the center of this path. It should be at least eight feet wide in its very narrowest points. And why not further distinguish it by a series of banners maybe 25 ft (8 m) apart, overhead along the length of the path, saying something like, "[STORE BRAND] EXPRESS - This way to convenient shopping?" The point is to open up the path - if you open it up, they will come - and then advertise innocuously what you have done.

You may notice that the return path here encompasses two aisles. I would suggest chopping that gondola that separates the two aisles down to a maximum of 5 ft tall, and put a "cut-through" half way down the aisle. These two measures will increase the open-ness of these aisles, and allow shoppers to move between them. Of course, simply removing the middle gondola would be very acceptable, as well, and would provide an ideal environment for six or eight "mid-caps" (See: Mid-Caps: Break Out of the Pack).

The point of all this is to stop running the store like a treasure hunt for the shopper, and instead to assist the shopper by providing a logical convenient path through the store - maintaining visual connection to the rest of the store - so that you can merchandise more intelligently, engineering your sales plan, step by step as the shopper moves along this path. That step by step sales plan will be the subject of a subsequent Views. But we will conclude this issue with the historical roots of this plan, and how it has actually been deployed in stores today, with as much as five times the sales of conventional supermarkets.

A massive shift in retailing occurred 100 years ago with the explosive growth of self-service retailing. Mass production, mass distribution with mass self-service created a mass market with large benefits for shoppers (more selection, lower prices, faster shopping,) retailers (greater efficiency, less staffing, "pile it high, and let it fly!") and suppliers (mass production, manufacturing and distribution efficiencies, and access to burgeoning markets!)

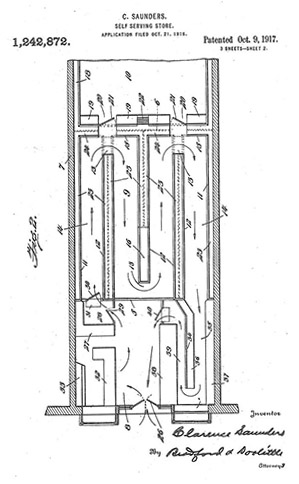

For retailers, the reduction or elimination of their sales team/staff, meant that their focus moved to logistics, supplier management/negotiations, and matching merchandise selection with their shoppers. No real selling was needed. Again, self-service means, "shopper, sell yourself." But the death of retailer selling (as contrasted with merchandising) was resisted by a few retailers. One in particular, Clarence Saunders, continually pressed for more efficiency in selling, and patented the store design represented here:

Notice the vestibule area at the front of the store, where shoppers can enter the display area, on the left, and pass in a serpentine path up and down a series of aisles. The purpose of this serpentine path was to allow the merchant to introduce the shopper to an "appropriate" offering of merchandise in a systematic way. In this way, Clarence Saunders retained control of the selling process, and was able to assist the shopper with their purchases. In effect, in these serpentine stores, the retailer assumed responsibility for selling, to an extent, instead of passively abdicating this responsibility for the sale to the shopper.

Obviously, instead of following this lead, retailers the world over abandoned Saunders' serpentine path, multiplied aisles, for which manufacturers generously rewarded them, and turned shoppers loose, to their own devices, in mini-warehouses. Retailers became passive in the process of shoppers making purchase decisions, essentially allowing selling skills to atrophy.

It is no wonder shoppers waste 80% of their time in the store, wandering about seeking something to buy - not to mention vast options when they finally arrive in an area where a purchase will actually occur. But there are modern incarnations of the serpentine store. Ikea is probably the best known global example. But for the CPG/FMCG market the pre-eminent example is Stew Leonards, where they achieve something like $100 million in sales with the serpentine path. HEB has Central Market stores following this model quite closely, presumably with similar results.

The U-turn path is just a simple form, a segment of the serpentine path, using the natural tendencies of shoppers, without the coercive restraint of path offered by Ikea, Stew Leonards and HEB Central Market. In fact, it is exactly the million-dollar per day model used by Costco. Any retailer who ignores the potential is probably addicted to the crack-cocaine of supplier payments, that obviate the need to care about lost selling skills.

In the next issue of the Views we will consider in some detail how to use the U-turn in shopping to efficiently sell to shoppers a greater volume of the merchandise they really want.